Market Report Plastics - October 2011

Information about the market for plastics is being presented by:

bvse - Bundesverband Sekundärrohstoffe und Entsorgung e.V.

1. The market for primary plastics

The criticism of the "pessimists of the banking industry" (cf. http://www.bdi.eu/Presse.htm), expressed by BDI President Keitel at the Day of Industry on 27th September,1 was bold, but none the less overdue. It seems that the highly speculative financial markets are, once again, getting in the way of the successful real economy. On the one hand, there is an increasing number of gloomy predictions of future economic developments; on the other hand, however, there is a great domestic and foreign demand for goods and services - at least in Germany.

The markets for primary plastics reflect the overall economic situation, which is, on the one hand, determined by the negative impulses of the financial markets and, on the other hand, by the considerable demand. The mood in the markets for standard plastics thus slightly deteriorated in September. Falling precursor prices as well as a restrained demand, which was accompanied by sufficient supply, led to price decreases. Thus, the EUWID Price Watch for standard plastics shows a decline in the prices of the standard plastics quoted - with the exception of HDPE blow moulding and PCV, which have held their own. The average price of the ten types of plastics listed below is 1332 /t. Thus, the plastics price has fallen short of the previous month's quote by 31 /t. The following prices were quoted in September: LDPE film grade 1350 - 1390 /t, LLDPE film grade 1240 - 1300 /t, HDPE injection moulding 1270 - 1320 /t, HDPE blow moulding 1270 - 1320 /t, PS crystal clear 1360 - 1400 /t, PS high impact 1490 - 1550 /t, PP homopolymer 1300 - 1390 /t, PP copolymer 1350 -1440 /t, PVC tube grade 1180 - 1220 /t and PVC film/cables 1280 - 1320 /t. The price of PET rose in September again! PET for packaging was quoted at 1570 - 1630 /t, which exceeded the previous month's quote by 25 /t. Notwithstanding the general trend of falling precursor prices, the rising quotes for PET are being attributed to the increased prices of specific precursors this month, too - especially those of PX (paraxylene) and those of MEG (monoethylene glycol). In September, the desired price increases in standard plastics could not be achieved. Experts expect the prices of standard plastics to decrease further in October.

2. The market for secondary plastics

The secondary plastics markets proved to be largely stable in September. Nevertheless, the market quotes were by rather varied: while the magazine "EUWID" continued the previous month's status quo for secondary plastics, the internet platform "plasticker" showed falling prices. The prospects of a potentially insecure economic situation have led to warehouse stocks being largely reduced in September and October. It is good to see that there is still sufficient demand for secondary plastics. Recyclates in particular are selling well along the entire product chain. Furthermore, consumer- and industry-oriented final products, which are in part made from plastics recylates, are still in very great demand.

According to the information provided by the Plastics Recycling Committee in the run-up to the 2011 ChinaReplas, which will be held in Guangzhou on 6th/7th November 2011, 20 million tons of plastics were recycled and processed in China in 2010, of which 8.6 million tons were imported. Just for comparison: according to the 2010 Consultic study, 2.1 million tons of plastics were recycled in Germany. It is becoming increasingly difficult to export plastics via Hong Kong to the People's Republic of China; there are plans to enhance the direct connection to this country. The dollar, which has increased again compared to the euro, is likely to give an additional boost to plastics exports to China.

2.1 EUWID Price Watch

According to EUWID, the September market for used plastics was rather calm and stable. The falling prices in the primary markets have not yet had a negative impact on the markets for secondary plastics. With the exception of a few post-user PE grades, the September quotes for standard plastics in the EUWID Price Watch held their own compared to the previous month.

The demand for PE post-industrial was stable in September, too. Regrind and bale goods were in great demand. The prices of post-user PE are reported to have risen by up to 30 /t - especially those of the export grades. For instance, the quotes for film have increased: LDPE shrink film natural (E40) 450 - 550 /t, LDPE shrink film mixed colours (E49) 250 - 330 /t, film transparent natural <70 ?m 330-380 /t, film transparent mixed colours <70 ?m 70-130 /t, mixed film (98/2) 330 - 380 /t, mixed film (90/10) 230 - 260 /t, mixed film (80/20) 200-220 /t and HDPE hollow bodies mixed colours (C29) 210 - 340 /t.

The demand for PP has increased in September and October, with the result that the decline in primary prices is not having any impact on secondary goods. High-grade PP recyclates are currently selling very well. The demand for PS is considerable at all levels. High-quality PS input for recycling into regrind, regranulates and compounds is in great demand. However, the processors' requirements regarding input quality are also increasing. According to EUWID, the demand for PVC is showing a tendency towards decline, but other indicators suggest that the demand for PVC is on the rise.

Post-user PET: The global trend towards using PET as packaging material is having a positive impact on PET recycling. At present, the existing recycling and processing capacities are being expanded. The domestic demand for PET recyclates is very high and is, in part, balanced out by imports. There is now, once again, an increased number of purchasing enquiries from the the Far East in the European markets. In September, the EUWID quotes decreased once again, namely by 20 /t. The following prices are now quoted for used and disposable PET bottles: PET transparent 440 - 500 /t and PET mixed colours 310 - 380 /t. To date, the price rises in the primary markets have hardly had any impact on the average bottle quotes mentioned here.

2.2 plasticker price index

In September, the demand for standard plastics was considerable throughout. However, the prices of standard plastics quoted in plasticker fell by 16 /t on average. These price decreases ranged between 20 /t and 150 /t, whereas the price rises were between 10 /t and 100 /t. LDPE bale goods and PS regranulates show longer-term trends towards declining prices, whereas the prices of PVC_U have risen. According to plasticker, the following price quotes changed by more than +/- 40 /t in September: HDPE regrind +50 /t, HDPE regranulates -50 /t, PP bale goods -100 /t, PP regrind -50 /t, PS regrind -60 /t, PS regranulates -150 /t, PVC_P regrind +90 /t and PVC_U regrind +100 /t. The forecast of the October Price Index shows stable prices and a considerable demand compared to August.

Table 1: Prices of standard plastics in plasticker, quoted in /t

*: Supply figures too low to attain statistical significance1: equivalent to the grade "post-industrial, mixed colours"; 2: equivalent to K49; 3: equivalent to K59; 4: equivalent to "standard, mixed colours"; 5: equivalent to "regranulates, black"

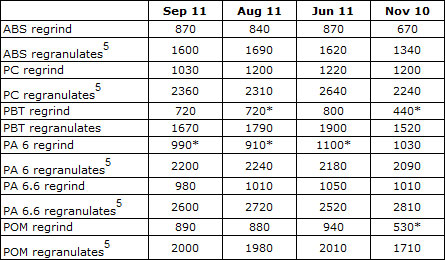

On the whole, the plasticker quotes for technical plastics decreased by 32 /t in September. The price reductions ranged between 30 /t and 170 /t, and there were price rises of 10 /t to 80 /t. Regranulates in particular were quoted at lower prices. In September, there was a large number of quotes for ABS regranulates, in which purchasers took a special interest. The following quotes changed by more than 70 /t in September: ABS regranulates -90 /t, PC regrind - 170 /t, PBT regranulates - 120 /t, PA 6 regrind +80 /t as well as PA 6.6 regranulates - 120 /t. The first forecast of the October quotes shows that the prices continue to be on the decline despite a sufficient demand.

Table 2: Prices of technical plastics in plasticker, quoted in /t

All EUWID prices are quoted ex works. As a rule, the prices quoted refer to quantities in excess of 20 tons. The monthly quotes for secondary plastics, which are updated on an hourly basis, can be calculated using the price lists that are derived from the quotations published in the raw material exchange plasticker. The prices listed in this index are quoted with reservation - as the majority of the quotes submitted are not necessarily equivalent to the sales prices. Furthermore, plasticker does not distinguish between the following grades: transparent, mixed colours or colour-separated. Therefore, the information provided by plasticker may indicate different market behaviour than the prices quoted by EUWID.