Market Report Plastics - July 2010

Information about the market for plastics is being presented by:

bvse - Bundesverband Sekundärrohstoffe und Entsorgung e.V.

1. The market for primary plastics

Even though the economic boom in the Far East continues, experts warn that the volume of orders is likely to stagnate medium term. Furthermore, the summer doldrums are having an impact. The prices of virgin material precursors, which have been decreasing in June and July, point in the same direction.Plastics processors have continued to suffer from the high plastics prices in July. According to the EUWID Price Watch for June, the existing reductions have led to further price rises in standard plastics. For some standard plastics, the supply-demand ratio has meanwhile improved considerably. The price rise that took place in June was less marked than in the previous months.

According to EUWID, the June Price Watch showed a price increase in standard plastics again, namely of 17 /t on average - with the exception of PS and PET. The price rise in standard plastics ranged from 10 - 50 /t. In June 2010, the average price of the ten types of plastics listed below was 1295 /t. The following prices were listed in the Price Watch for the ten types of standard plastics: LDPE film grade 1340 - 1370 /t, LLDPE film grade 1320 -1360 /t, HDPE injection moulding 1210 - 1240 /t, HDPE blow moulding 1200 - 1230 /t, PS general purpose 1330 - 1370 /t, PS high impact 1400 - 1450 /t, PP homopolymer 1340 - 1400 /t, PP copolymer 1390 - 1450 /t, PVC tube grade 1080 - 1120 /t and PVC film/cables 1130 - 1170 /t. The PS prices decreased, namely by 20 - 40 /t. The price of PET for packaging fell short of the previous month's quote by 35 /t, i.e. it was quoted at 1260 - 1370 /t. Thus, the PET prices decreased for the first time in several months.

As far as technical plastics are concerned, the upward trend still continues. In the EUWID Price Watch for June, all technical plastics were quoted at a higher price than in April. Here the price rises ranged from 50 /t to 300 /t. The following prices were quoted: PMMA crystal clear 2300 - 2400 /t, ABS natural 1650 - 1750, ABS white/black 1730 - 1850, ABS mixed colours 2350 - 2600, PC crystal clear 2650 - 2800 /t, PC GF 2850 - 3000 /t, POM natural 2050 - 2150 /t, PA 6 natural 2150 - 2300 /t, PA 6 black 2150 - 2300 /t, PA 6 GF reinforced 2300 - 2400 /t, PA 66 natural 2900 - 3050 /t and PA 66 GF 3000 - 3150 /t. The demand for technical plastics is, in part, still accompanied by a shortage of supply. Even though experts expect the volume of orders to decline during the summer break, there will still be a considerable demand for technical plastics. This ultimately indicates price stabilisation, too - albeit with a certain time lag.

In week 27 the PP and LLDPE prices for Europe on the London Metal Exchange (LME) were quoted as follows: the PP purchase prices for July, August and September were at USD 1315 respectively, whereas those of LDPE were at USD 1400 respectively. Thus the August quotes for PP were reduced by 25 USD/t, whereas those of LLDPE decreased by 50 USD/t. Hence, the prices quoted on the London Metal Exchange (LME) are more varied. In other words, this indicates the end of the general price boom. Certain quotes are likely to further increase in the next few months. However, price reductions can also be observed at the same time. Experts continue to assess the demand for plastics as being high; however, the supply quantities are also increasing.

2. The market for secondary plastics

The demand from the primary plastics market has continued to revive the secondary markets in June and July. The input prices of processing bale goods and regrind have increased to a lesser extent. High-quality plastics recyclates, regrind and regranulates in particular, are selling well, as these offers perfectly supplement the primary goods. The demand for exports from the Far East is high; however, the demand for film is in part no more than sluggish. To date, the company holidays in July have led to price stabilisation - and this trend is likely to continue in August, too.

2.1 EUWID Price Watch

The EUWID Price Watch for June shows price increases in numerous types of plastics, above all in regrind, namely of 10 - 80 /t, whereas the quotes for thin film and mixed film have decreased by 10 - 40 /t. All in all, the occasional price reductions, which are offset by the price rises, ultimately indicate market stabilisation. On the whole, the market is characterised by a great domestic demand.

PE: As far as post-industrial waste is concerned, PE shows price increases, whereas the prices of post-user PE either increase or decrease. The price increases in PE post-industrial range from 10 - 50 /t. Thus, the following prices were quoted in June: HDPE mixed colours 400 - 520 /t, HDPE natural 500 - 630 /t, LDPE mixed colours 370 -470 /t, LDPE natural 500 - 650 /t and LDPE film grade natural (K40) 400 - 530 /t. Post-user PE was quoted as follows: LDPE shrink film natural (E40) 430 - 470 /t, LDPE shrink film mixed colours (E49) 220 - 290 /t, film transparent natural < 70 µm 280 - 320 /t, film transparent natural < 70 µm 30 - 60 /t, LDPE farm film black/white > 70 µm 20 - 60 /t, PE mixed film (98/2) 280 - 320 /t, PE mixed film (90/10) 190 - 220 /t, PE mixed film (80/20) 170-200 /t and HDPE regrind from crates mixed colours 400 - 460 /t. The prices of thin film as well as mixed film and farm film decreased, namely by 5 - 40 /t, depending on the grade. Thick film showed price stabilisation or slight increases.

PP: PP post-industrial shows numerous price increases, namely of 30 - 80 /t. The June quotes changed as follows: film natural 300 - 350 /t, homopolymer mixed colours 400 - 500 /t, homopolymer natural 450 - 650 /t, copolymer mixed colours 400 - 500 /t and copolymer natural 450 - 650 /t. The shortage of supply is accompanied by a great demand from the primary and secondary markets.

PS: The prices of PS post-industrial have held their own. The prices on the primary markets, which have decreased by 20 - 50 /t, have led to price stabilisation on the secondary markets.

PVC: Even the June Price Watch showed price increases in all PVC grades again, namely of 20 - 50 /t. The following prices were quoted for PVC post-industrial in June: PVC_P transparent 370 - 450 /t, PVC_U mixed colours 340 - 400 /t, PVC_U mixed colours 350 -430 /t and tube grade mixed colours 300 - 400 /t. The following prices were quoted for PVC windowframe regrind: windowframe regrind white 500 - 620 /t, windowframe regrind mixed colours 370 - 450 /t and windowframe regrind single-shade white 620 - 770 /t. The considerable building activity has led to a satisfactory reduction in PVC tubes and windows.

PET post-user: Is the PET market tilting? Only to a very limited degree are the recyclers willing to pay the considerable PET prices. Production capacity may be reduced. However, the processors speculate that the situation will ease in July and August - on the one hand, because the bottle supply available has increased considerably and is likely to further rise as a result of the weather, i.e. the large number of hot days. On the other hand, the PET virgin material prices are meanwhile decreasing markedly. Furthermore, experts report that the demand from the Far East has fallen.

Ever since August 2009, the PET prices have been steadily rising. In June, the PET market was characterised by a further price increase. Hence, EUWID then quoted the following prices for used and disposable PET bottles: PET tranparent 400-450 /t and PET coloured 220-260 /t. This means that the price of PET transparent increased by 10 - 20 /t, whereas the quote for PET coloured rose by 10 /t on average. Coloured PET bottles also attained record prices.

2.2 plasticker price index

The evaluation of the data derived from the plasticker price index for June reveals a price increase in all standard plastics, even though there were two price reductions, namely in LDPE bale goods ( - 20 /t) and LDPE regranulates (- 10 /t). The following price changes of greater than/less then 40 /t can be reported for June 2010 compared to May 2010: HDPE bale goods + 110 /t, HDPE regranulates + 90 /t, LDPE regrind + 90 /t and PS regranulates + 60 /t. The first forecast of the July quotes indicates price stabilisation or slightly rising prices.

Secondary standard plastics

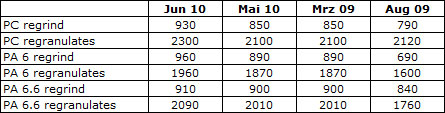

In June, technical plastics showed markedly higher quotes for regrind and regranulates. The increases in regrind ranged from 10 /t to 80 /t and those in regranulates from 80 /t to 200 /t. The first forecast of the June quotes indicates price stabilisation. Thus, the secondary markets for technical plastics follow the trends on the primary markets.

Secondary technical plastics

*Supply figures too low to attain statistical significance

The quotes for secondary plastics, which are updated on an hourly basis, can be calculated using the price lists that are derived from the quotations published in the raw material exchange plasticker. The prices listed in this index are quoted with reservation - as the majority of the quotes submitted are not necessarily equivalent to the sales prices.Therefore, the information provided by plasticker indicates distinctly different market behaviour than the prices quoted by EUWID.

The EUWID price quotes refer to bale goods or regrind. The given prices were quoted for business transactions between sorting plants and sales agents or the processing industry, as the case may be. As a rule, prices refer to quantities in excess of 20 to ex works. The prices attainable in trade can differ considerably from the indicated price range in both directions, depending on the grade of the type of plastic material quoted. The abbreviations used for some grades refer to the list of waste plastics published by the German Federal Association for Secondary Raw Materials and Waste Disposal (bvse)/Bureau of International Recycling (BIR).